VA Home Loans in the DMV: What Veterans Need to Know in 2026

The DMV is one of the largest concentrations of veterans, active-duty service members, and military families in the country. The Pentagon, Joint Base Andrews, Fort Belvoir, Quantico, Fort Meade, the Naval Academy, the Coast Guard Yard, NSA Fort Meade, Walter Reed — within a one-hour drive of Annapolis you can hit a half-dozen of the largest defense and intelligence installations in the United States.

And yet a meaningful share of DMV veterans who qualify for a VA home loan never use it. Others use it once and assume they're done. The VA loan is one of the strongest mortgage products in the country, especially in a high-cost market like the DMV, and the 2026 rules are worth understanding before you write your next offer.

Why the VA loan matters most in markets like the DMV

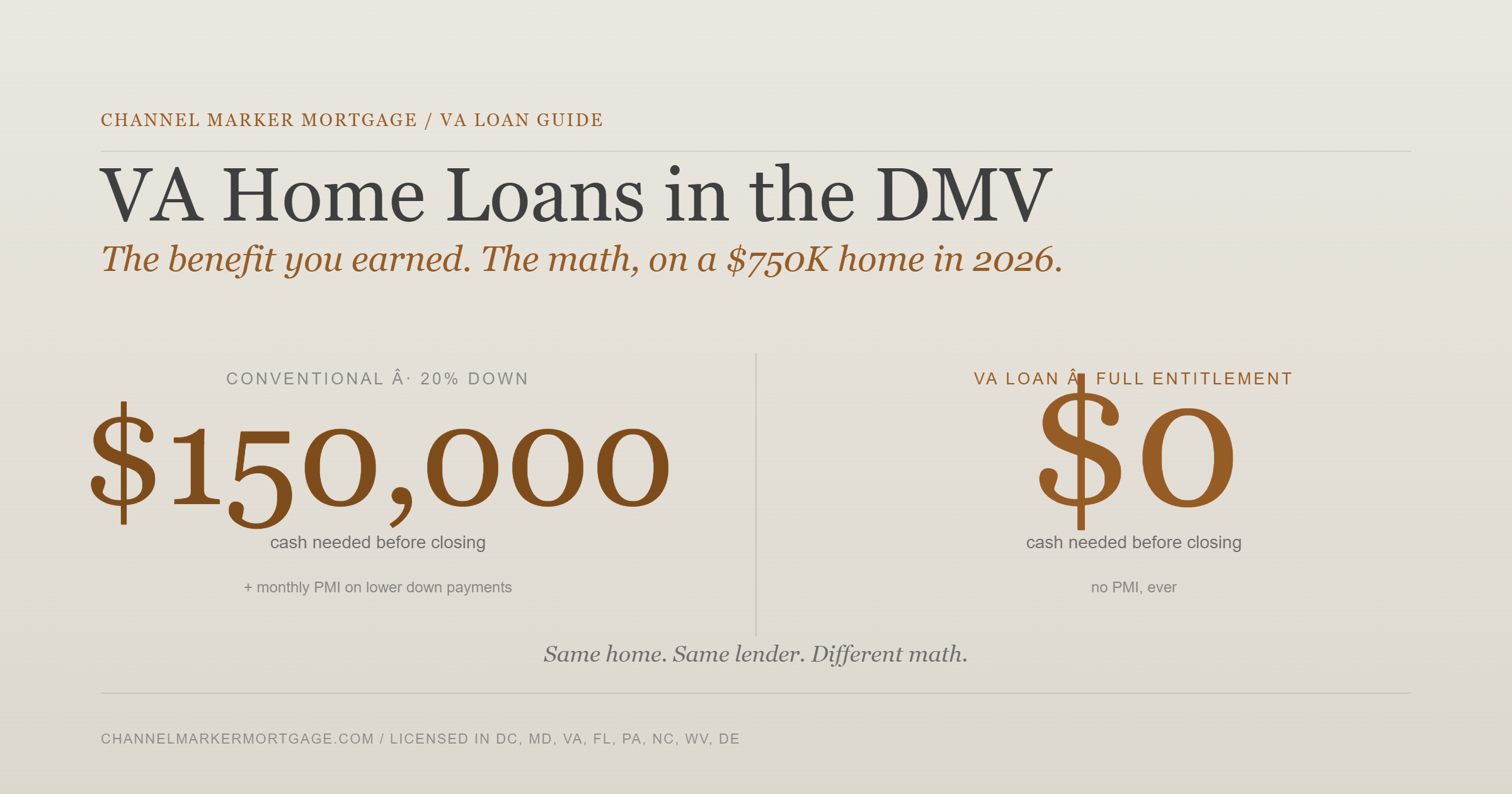

The headline benefit is the one most buyers know: zero down payment, no private mortgage insurance, and competitive interest rates. In a market where a starter townhouse in Arlington or Silver Spring can run $700,000, the practical effect is enormous.

A conventional buyer putting 20% down on a $750,000 home needs $150,000 in cash before they ever sit at the closing table. The same buyer with full VA entitlement needs zero. Even a 5% conventional down payment on that same home is $37,500 — plus monthly PMI that runs $200–$400 a month until you've built 20% equity.

VA financing collapses both numbers to zero. For active-duty service members who PCS every two to three years, that's the difference between buying and renting in nearly every assignment.

How the VA loan actually works in 2026

A VA loan is issued by a private lender — Channel Marker, a credit union, a bank — and guaranteed by the Department of Veterans Affairs. The VA isn't lending the money; it's standing behind it, which is why the rates are so competitive and the underwriting is so much more flexible than conventional financing.

In addition to the zero-down feature, VA loans offer:

No PMI. Conventional loans with less than 20% down require monthly mortgage insurance. VA loans never do, regardless of equity.

Lower rates. VA rates typically run 0.25%–0.50% lower than comparable conventional rates because of the federal guarantee.

Looser DTI and credit guidelines. A VA loan can underwrite to higher debt-to-income ratios and lower credit scores than a conventional loan — useful for younger service members and recent retirees still rebuilding civilian credit.

Up to 4% in seller-paid concessions. On top of the standard 6% closing-cost concession allowed across most loan types, VA buyers can negotiate up to an additional 4% to cover the funding fee, prepaid taxes, or even existing debts the seller pays off at closing. It's the most generous concession ceiling of any major loan product.

VA loan limits in 2026 — and why they probably don't apply to you

Since 2020, VA loans have had no upper limit for borrowers using their full entitlement for the first time. This is the rule that actually matters for most DMV buyers. If you've never used your VA benefit, or if you've sold a previous VA-financed home and restored your entitlement, you can buy at any price your income supports.

If you have partial entitlement — meaning you have an active VA loan you're keeping or sold a VA home through assumption — you're limited by the conforming loan ceiling for your county. In 2026, that ceiling is $1,249,125 in DC, Montgomery County, Fairfax, Arlington, Loudoun, and Prince William, and $832,750 in lower-cost DMV counties. Most DMV homes fit comfortably under those caps.

The VA funding fee — and the exemption most disabled vets miss

The VA funding fee is a one-time charge that replaces the PMI a conventional borrower would pay every month. With zero down on a first-time use, it's 2.15% of the loan amount. On a subsequent use it climbs to 3.30%. Putting down 5% drops the fee to 1.50%; 10% or more drops it to 1.25%.

On a $750,000 zero-down purchase, that first-use fee is $16,125. For a vet using the benefit a second time, it's $24,750. Real money — and worth knowing two facts about:

You can finance the fee into the loan rather than pay it at closing.

You may be fully exempt. Veterans receiving service-connected disability compensation at any rating — even a 10% rating — are exempt from the funding fee. Surviving spouses receiving DIC, Purple Heart recipients on active duty, and certain medically-discharged veterans are also exempt. We see DMV veterans paying tens of thousands of dollars in funding fees they didn't owe, often because their loan officer didn't ask the right question. Always confirm your VA disability status before you write an offer.

Common DMV VA loan questions

Can I use my VA loan while still on active duty? Yes. Most active-duty PCS moves are financed with VA loans.

Can I buy an investment property? No. VA loans require you to occupy the home as your primary residence within 60 days of closing.

Can I have two VA loans at once? Yes, with sufficient remaining entitlement. Common scenario: a service member buys at one duty station, PCSes, and uses remaining entitlement to buy at the new station while renting out the first.

Can my spouse use my benefit? Surviving spouses can. Spouses of living veterans can co-sign and have their income counted, but the COE belongs to the veteran.

What about refinancing? The VA Interest Rate Reduction Refinance Loan (IRRRL) is one of the simplest refinance products in mortgage — minimal underwriting, no appraisal required in most cases.

What to do next

If you're a DMV veteran or active-duty service member ready to buy, three steps:

Pull your Certificate of Eligibility through the VA's eBenefits portal. It's instant for most service records.

Confirm your VA disability status before applying — the funding fee exemption can save you five figures.

Get a real loan estimate from a lender who actually closes VA loans regularly. The VA process has nuances (especially around appraisal contingencies and pest inspection requirements) that loan officers who don't work with VA buyers regularly will fumble.

Channel Marker Mortgage is a multi-state mortgage broker licensed in DC, Maryland, Virginia, and five other states. We work with VA buyers across every DMV duty station, and we don't outsource the underwriting to a call center two time zones away.

Book a 15-minute call and we'll walk through your benefit, your funding-fee exemption, and what your number actually looks like in the market you're shopping.

VA loan rules, funding fee schedules, and county loan limits referenced in this post reflect the Department of Veterans Affairs guidelines in effect for 2026. Programs and limits change. Verify current figures with your lender or the VA before relying on them for a transaction. Channel Marker Mortgage is not affiliated with the Department of Veterans Affairs and is not a government agency.

Closing Costs in DC, Maryland & Virginia: What Buyers Actually Pay in 2026

A buyer purchasing a $750,000 home in Bethesda will write a different check at the closing table than a buyer purchasing the same $750,000 home in Arlington — or in Capitol Hill. Sometimes the difference is more than $10,000. The home is the same. The lender can be the same. The closing costs are not.

If you're shopping across the DMV, this is one of the most important numbers most buyers don't think about until the loan estimate lands in their inbox. Here's what to expect in DC, Maryland, and Virginia in 2026 — and why the differences are larger than most buyers realize.

Why DMV closing costs are unusual

In most metros, "closing costs" mean roughly the same thing whether you're shopping in one suburb or another. Not in the DMV. Three separate jurisdictions overlap in a single metropolitan area, and each writes its own rules for transfer taxes, recordation taxes, and first-time-buyer exemptions. A buyer comparing a townhouse in Falls Church to a townhouse in Silver Spring is comparing two different tax regimes — even if the home prices are identical.

The biggest swings show up in three line items: state and local transfer taxes, recordation taxes, and first-time-buyer exemptions. Lender fees, appraisal, and title insurance are roughly comparable across the three. The transfer and recordation taxes are not.

Maryland: mid-range, but the county matters

Maryland buyers pay a 0.5% state transfer tax plus a county transfer tax that varies by jurisdiction — Montgomery County charges 1.0%, Howard County 1.0%, Anne Arundel 1.0%, and Prince George's 1.4%. On top of that, Maryland charges a state recordation tax of roughly $5.00 per $500 of the purchase price (about 1.0% effective).

Customary practice in Maryland is to split transfer and recordation taxes equally between buyer and seller, but this is negotiated in every contract. As a buyer, plan on roughly 1.25% to 1.7% of purchase price in transfer and recordation costs alone, depending on county and how the contract is written.

First-time Maryland homebuyers get a meaningful break: they're exempt from the buyer's half of the 0.5% state transfer tax. That's roughly $1,875 saved on a $750,000 purchase — small, but worth claiming.

Virginia: the lowest closing costs in the DMV

Virginia is the cheapest jurisdiction to close a purchase in. The state recordation tax is roughly 0.25% on the deed, plus a grantee tax of about 0.083%, plus a small local recordation tax of another 0.083%. Total buyer-side transfer and recording costs come in around 0.42% of purchase price — meaningfully lower than either Maryland or DC.

There's one wrinkle for Northern Virginia: counties subject to the regional congestion relief tax (Fairfax, Arlington, Alexandria, Loudoun, Prince William, and others) add roughly 0.10% — but this is paid by the seller, not the buyer.

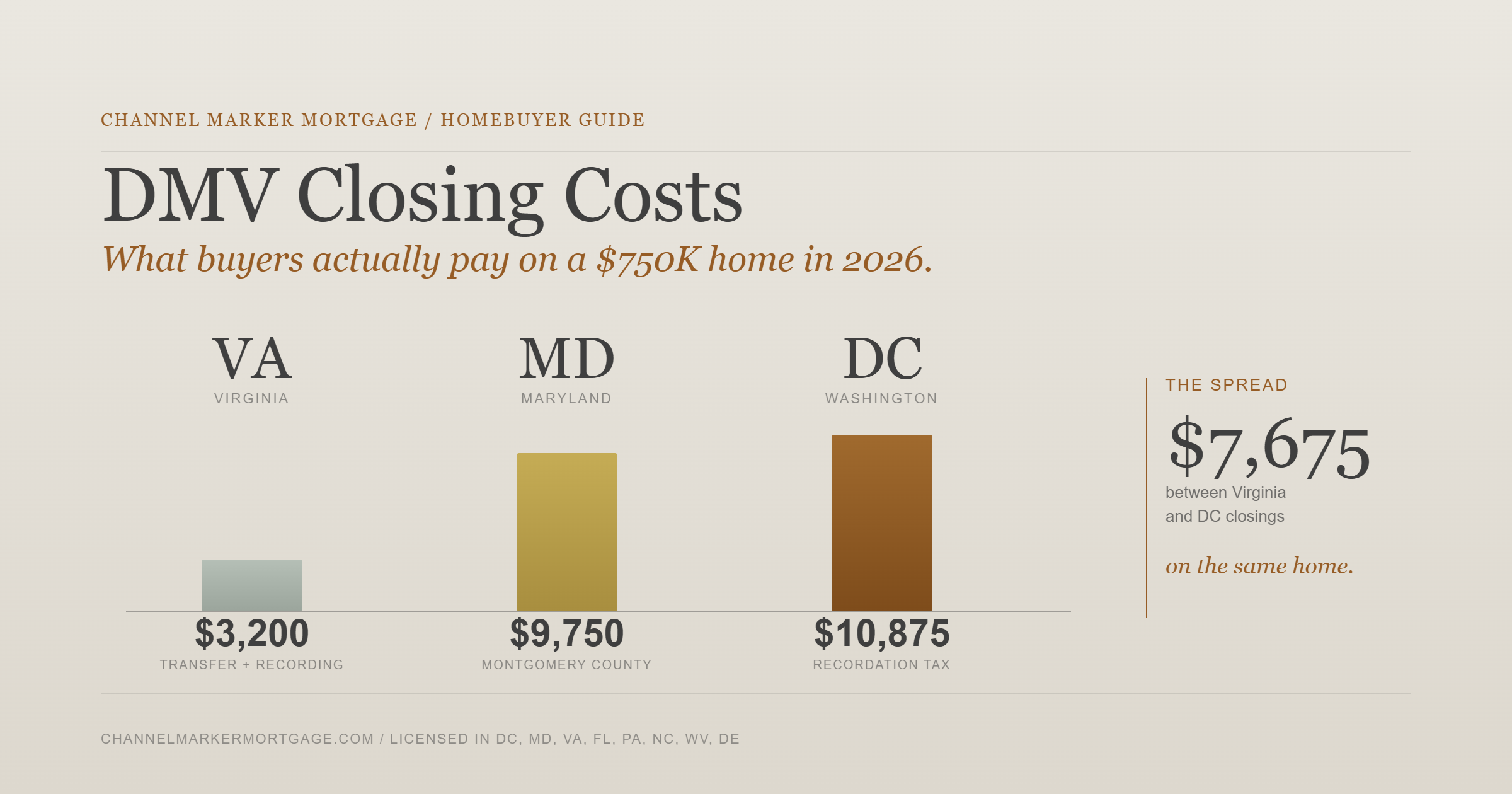

For buyers stretching to make a number work, this can be a real factor. A $750,000 home in Arlington costs the buyer roughly $3,000–$3,500 in transfer and recordation. The same purchase in Montgomery County costs the buyer closer to $9,500–$13,000 once county transfer is split.

DC: the highest closing costs of the three

DC has the highest transaction taxes in the DMV. The DC recordation tax is paid by the buyer at 1.1% of purchase price for homes under $400,000 and 1.45% for homes $400,000 and above. The DC transfer tax is paid by the seller at the same rates — but is sometimes negotiated as a buyer concession.

On a $750,000 DC purchase, recordation alone is $10,875. That's the buyer's line item, before any lender or title fees.

The good news: first-time DC homebuyers can claim a reduced recordation tax of 0.725% (versus 1.45%), provided they meet the income and ownership-history requirements. On the same $750,000 purchase, that's a savings of roughly $5,400. If you're a first-time DC buyer, this exemption is worth structuring your offer around.

Side-by-side: $750,000 home, buyer-side closing costs

Arlington, VA: ~$3,200 — Lowest in the DMV

Montgomery County, MD: ~$9,750 — Assumes 50/50 split per custom

Washington, DC: ~$10,875 — Drops to $5,440 for first-time buyers

These numbers exclude title insurance (typically 0.5–1.0%), lender fees, prepaid taxes and insurance, and appraisal. Add roughly 2–3% of purchase price total when budgeting for buyer closing costs across the DMV — and use the higher end if you're closing in DC or a high-county-transfer Maryland jurisdiction.

What this means for your offer

If you're shopping across state lines, factor closing costs into your budget the same way you factor interest rate or property tax. A buyer who can stretch to $800,000 in Arlington may only be able to stretch to $775,000 in Bethesda once the transfer math is done.

If you're a first-time buyer in DC, claim the reduced recordation rate. It's the single largest concession available to you, and it's only granted at closing if your contract requests it.

If you're buying in a high-transfer Maryland county, negotiate the split. The 50/50 convention is exactly that — a convention. In a soft market, sellers will often absorb more.

If you're stretching budget, ask your lender for a side-by-side estimate before you write an offer. The loan estimate is a federal disclosure that has to land in your inbox within three days of application — and the closing-cost line items are the most negotiable parts of the entire transaction.

Get a real number, not an estimate

Online closing-cost calculators get you in the right ballpark. They miss the local nuances — first-time-buyer programs, county-specific rates, lender credits, and seller concessions — that move the number by thousands.

Channel Marker Mortgage is licensed across DC, Maryland, Virginia, and five other states, and we run real loan estimates for every jurisdiction in the DMV. If you're trying to figure out which side of the river makes the most sense for your purchase, we'll model both — same lender, same loan, side-by-side numbers — so you can write the offer with confidence.

Book a 15-minute call and we'll walk you through your numbers.

The transfer, recordation, and grantee tax rates in this post reflect 2026 schedules in the District of Columbia, the State of Maryland (including Montgomery, Howard, Anne Arundel, and Prince George's Counties), and the Commonwealth of Virginia. Rates and exemption thresholds change. Verify current figures with your lender or settlement attorney before relying on them for a transaction.

Home Loans in Annapolis, MD: A Local Mortgage Broker’s 2026 Guide

Buying a home in Annapolis isn’t like buying anywhere else in Maryland. Median home prices have settled around $650,000–$660,000, the buyer pool leans heavier on military families, Naval Academy connections, and D.C. commuters than markets further inland, and the housing stock runs from $400K Cape St. Claire ranchers to $2M+ waterfront estates in Eastport and downtown.

Choosing the right home loan matters more here than in markets where one or two products fit almost everyone. I’ve been a mortgage advisor in this market since 2013 — this is the guide I wish more buyers got before they started touring homes.

Plain English. Local context. No jargon.

What Makes the Annapolis Market Different

Prices push more buyers into jumbo territory than most Maryland markets. The 2026 conforming loan limit in Anne Arundel County is $832,750. A meaningful chunk of Annapolis purchases hit that threshold and need to be structured caVA Loans

If you’re eligible — active duty, veteran, or a qualifying surviving spouse — VA is almost always the right answer. No down payment, no PMI, rates that consistently run 0.375%–0.5% below conventional, and the 2026 entitlement rules let qualified veterans finance well above the conforming limit with $0 down. We covered the deeper details in our VA Home Loan Benefits Explained post.

The Home Loan Options That Matter in Annapolis

Conventional / Conforming Loans

The default for buyers with 5%+ down and a credit score above 620. In 2026, the conforming limit in Anne Arundel County is $832,750. If you’re staying under that number, conventional financing is almost always on the table and is usually the cleanest path. Above it, you’re in jumbo territory.

Jumbo Loans

If you’re buying in Eastport, downtown Annapolis, on the Broadneck peninsula, or anywhere on the water, you’re very likely looking at a jumbo. Jumbos typically require stronger reserves and a credit score in the 700s, but pricing has become aggressive over the last 18 months. We’ve structured Annapolis jumbos up to $3M+ — and the rate spread between conforming and jumbo is the smallest it’s been in years.

FHA Loans

Best fit for buyers with credit scores in the 580–680 range, or anyone short on down payment. FHA allows as little as 3.5% down. The FHA limit in Anne Arundel County for 2026 is $805,000 for a single-family home — enough to buy in most surrounding submarkets, but tight for downtown or waterfront.

USDA Loans

Most of central Annapolis isn’t USDA-eligible, but parts of Anne Arundel County — the more rural pockets toward the south, Davidsonville, Mayo, and parts of Crownsville — qualify for $0-down USDA financing. Worth checking the eligibility map before you write off the option.

Bridge / Buy-Before-You-Sell Loans

Annapolis has a real “moving up the rung” pattern — sell the starter home in Bowie or Glen Burnie, buy the family home in Cape St. Claire, Arnold, or Severna Park. Bridge loans and Buy-Before-You-Sell programs let you make a non-contingent offer on the new house before you’ve sold the old one. In a market this competitive, that’s often the difference between landing the home and losing it.

The Five-Question Decision Framework

What's the right home loan for you? Answer these five questions and you're 80% of the way there:

Am I military-eligible? Run the VA numbers first, always.

Am I above the $832,750 conforming line? If yes, jumbo strategy comes into play.

Do I have less than 10% down? FHA, down payment assistance, or a low-down-payment conventional are all worth comparing.

Am I selling another home to fund this one? Bridge or Buy-Before-You-Sell.

If refinancing — what rate is on my current mortgage? Your existing rate matters more than today's headline rate.

The right answers depend on your full picture — credit, reserves, income structure, timeline. A 15-minute conversation gets us most of the way there.

What to Do Before You Start Touring Homes in Annapolis

A few things that meaningfully change outcomes in this market:

Get a fully underwritten pre-approval, not a pre-qualification. In Annapolis, good homes get multiple offers in a weekend. A real underwriter sign-off — not just a desktop estimate — gives your offer cash-equivalent strength.

Know your true monthly payment, not just your purchase price. Anne Arundel County property taxes plus homeowners insurance can run $700–$1,200/month on top of principal and interest. Backing into the mortgage from the monthly is more honest than backing into the monthly from the mortgage.

Know your closing costs to the dollar. Maryland's recordation and transfer taxes are higher than most states. We walk every client through the numbers line-by-line so there are no surprises at the table.

Work with a local mortgage advisor, not a 1-800 number. Annapolis appraisers, listing agents, and title companies operate on their own rhythms. Local relationships close loans faster — our average is 11.5 days from application to clear-to-close, well under industry norms.

The Bottom Line

Annapolis is one of the best places to own a home anywhere in the Mid-Atlantic. But the loan you put on it can save or cost you tens of thousands of dollars over the life of the mortgage. Channel Marker Mortgage is a local, multi-state brokerage built on the idea that buyers in this market deserve the same access to wholesale pricing as the biggest accounts in the country — and the kind of hands-on service you can't get from a national call center.

If you're shopping for a home in Annapolis, let's talk before you write your first offer.

VA Home Loan Benefits Explained — And Yes, You Can Have More Than One

If you've served in the military, you've earned one of the most powerful mortgage benefits in existence: the VA home loan. Yet a surprising number of veterans in the Annapolis area either don't use it, or don't fully understand it.

Here's what it is, what it gets you, and — to answer the question we hear all the time — yes, you can have more than one.

What Is a VA Home Loan?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs. The VA doesn't lend money directly — instead, it guarantees a portion of your loan, which gives lenders the confidence to offer terms that simply aren't available through conventional financing.

The result: eligible veterans and service members can buy a home with none of the usual barriers.

The Benefits Are Hard to Beat

• No down payment required — buy a home with $0 down in most cases

• No private mortgage insurance (PMI) — ever. This alone saves hundreds per month on a typical Annapolis-area home

• Lower interest rates — VA loans consistently run 0.375%–0.5% below conventional rates

• Flexible credit requirements — the VA sets no minimum credit score; most lenders work with 580+

• No prepayment penalty — pay it off early with no fees

• Lifetime benefit — it doesn't expire and can be used multiple times

On a $600,000 home — close to the Annapolis median — skipping PMI and getting a lower rate could save a veteran $400–$600 per month compared to a conventional loan. Over 30 years, that's real money.

Who Qualifies?

VA loan eligibility is based on your military service history. In general, you may qualify if you are:

• A veteran who served 90 consecutive days of active duty during wartime, or 181 days during peacetime

• An active-duty service member with at least 90 continuous days of service

• A National Guard or Reserve member with 6 years of service, or 90+ days of active-duty deployment

• An eligible surviving spouse of a service member who died in the line of duty or from a service-connected disability

To confirm your eligibility, you'll need a Certificate of Eligibility (COE). Your lender can pull this electronically in minutes — you don't need to have it in hand before starting the process.

Can I Have More Than One VA Loan?

This is the question we get asked most often — and the answer surprises a lot of veterans: yes, you can.

Your VA loan benefit is a lifetime entitlement, not a one-time coupon. There is no cap on how many VA loans you can use over the course of your life. And under certain circumstances, you can hold two VA loans at the same time.

How It Works: VA Entitlement

The key concept is entitlement — the amount the VA guarantees to your lender. Think of it as a guarantee fund rather than a loan cap. When you use a VA loan, a portion of your entitlement gets tied up in that property. Once you sell the home and pay off the loan, your entitlement is restored and you're back to full benefit.

But here's what many veterans don't realize: if you still have remaining entitlement after your first VA loan, you can use it again — even while the first loan is still active. This is called second-tier entitlement.

When Can You Hold Two VA Loans at Once?

The most common situation is a Permanent Change of Station (PCS) order. If you receive military orders and need to relocate before you can sell your current home, the VA loan program is built for exactly this scenario. You can keep your current VA-financed home — often renting it out — and purchase a new primary residence using your remaining entitlement.

Other situations where a second VA loan may be possible include job relocation or a significant change in family circumstances. What the VA doesn't allow: using the benefit purely to buy investment or vacation properties. Each VA loan must be for a home you intend to occupy as your primary residence.

What If You've Used Your VA Loan Before and Want to Use It Again?

You have options depending on your situation:

• Sold the home and paid off the VA loan: Your entitlement is fully restored. You're back to $0-down eligibility on the next purchase.

• Still own the home but have remaining entitlement: You may be able to purchase again with no down payment if your remaining entitlement covers 25% of the new loan.

• Entitlement doesn't fully cover 25% of the new loan: You're not disqualified — you may simply need a small down payment to bridge the gap.

• Paid off a VA loan but kept the home: You can request a one-time entitlement restoration to reuse the benefit.

VA Loans in Annapolis: What You Should Know

Annapolis and Anne Arundel County are well-suited for VA buyers. With a significant military and veteran population — driven by the Naval Academy and proximity to multiple installations — the local market is familiar with VA transactions. Most sellers and real estate agents in the area understand VA appraisals and timelines.

One thing to keep in mind: Annapolis median home prices are around $650,000–$660,000. Veterans with full entitlement have no loan limit and can finance above the 2026 baseline conforming limit of $832,750 — meaning you won't hit a ceiling on the VA benefit in most Annapolis transactions.

Ready to explore you eligibility?

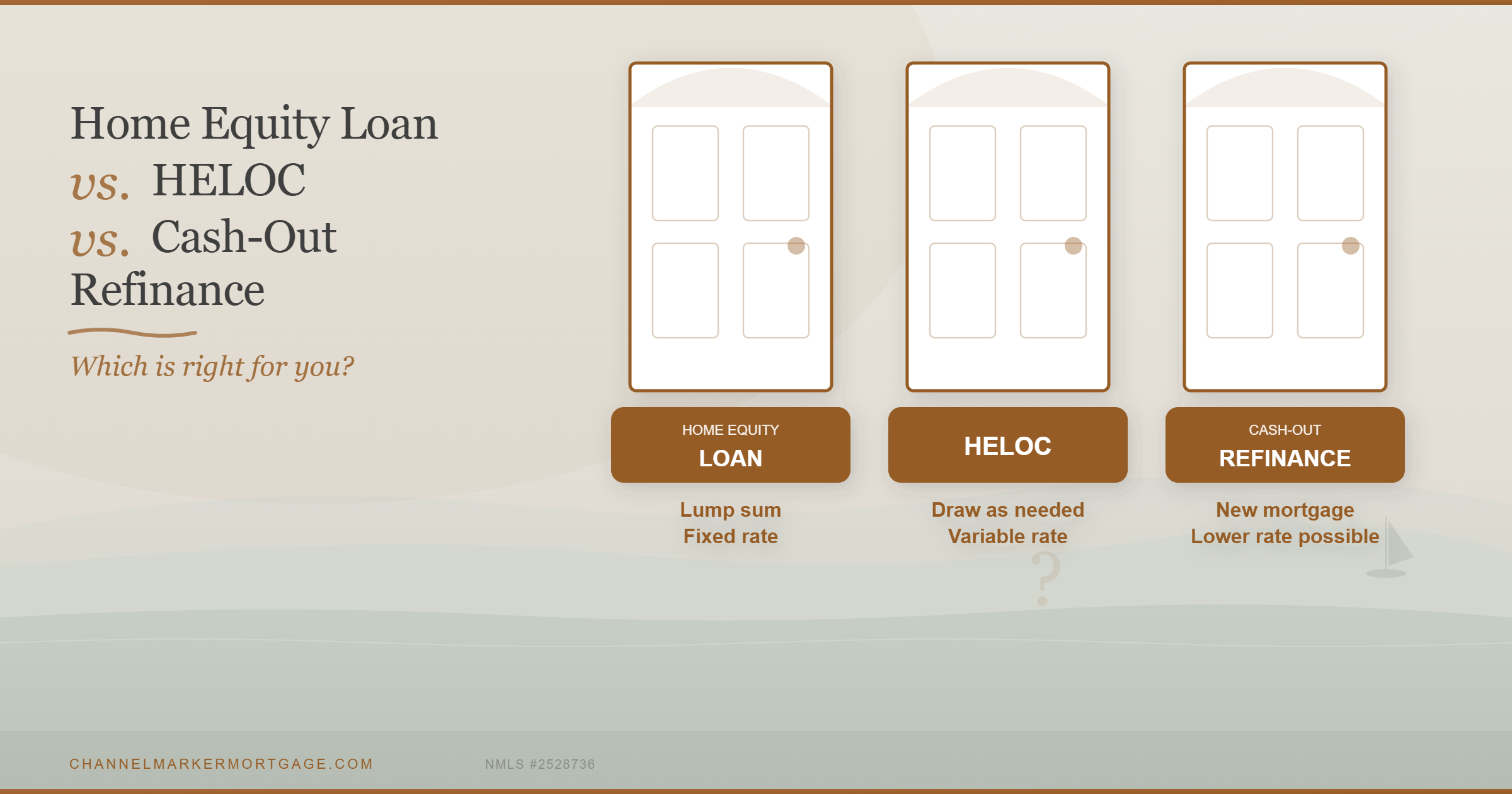

Home Equity Loan vs. HELOC vs. Cash-Out Refinance: Which Is Right for You?

If you own a home in Annapolis, there's a good chance you're sitting on significant equity. Median home values are hovering around $650,000-$660,000 — which means many local homeowners have six figures available to put to work. The real question is how to access it wisely.

Three options: a home equity loan, a HELOC, and a cash-out refinance. Each works differently. Here's the plain-English breakdown.

At a Glance

| Home Equity Loan | HELOC | Cash-Out Refinance | |

|---|---|---|---|

| Funds | Lump sum | Partial Lump Sum then draw as needed | Lump sum |

| Rate | Fixed | Variable | Fixed |

| Your mortgage | Unchanged | Unchanged | Replaced |

| Avg. rate* | ~8.0% | ~7.25% | ~6.5% |

| Closing costs | Moderate | Low | 2%–5% of loan |

*National averages, April 2026. Your rate depends on credit score and equity.

Home Equity Loan

A lump sum at a fixed rate, repaid in equal monthly installments. Your existing mortgage stays exactly as-is. Best if you know exactly how much you need and want payment certainty — a kitchen remodel, a debt payoff, a major one-time expense.

HELOC

A revolving line of credit secured by your equity — draw what you need, when you need it, and only pay interest on what you use. The rate is variable, so payments can shift. Best for ongoing projects, uncertain costs, or homeowners who want a financial safety net without a fixed monthly obligation.

Cash-Out Refinance

You replace your existing mortgage with a new, larger home mortgage loan and pocket the difference. You end up with one loan and one payment. The rate is lower than a home equity loan — but you're refinancing your entire mortgage, which only makes sense if today's rate is competitive with what you already have.

The One Question That Decides It

What rate is on your current mortgage?

• Below 5%: Use a home equity loan or HELOC. Protect your primary rate.

• Above 6.5%: A cash-out refinance is worth comparing — you may be able to lower your rate and get cash at the same time.

Not sure? That's exactly what we're here for.

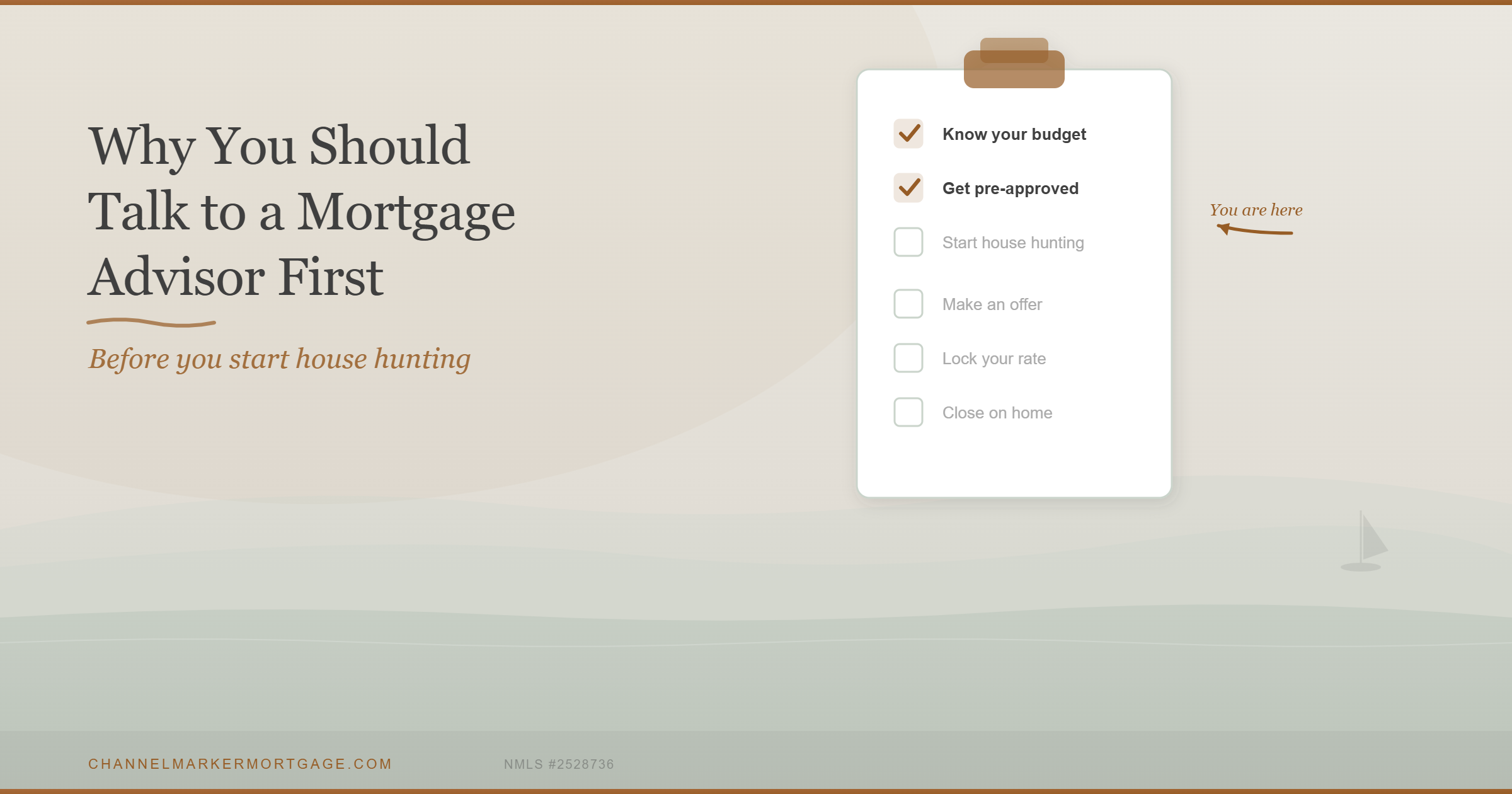

Why You Should Talk to a Mortgage Advisor Before You Start House Hunting

Most homebuyers start by browsing listings online or attending open houses. The smartest buyers start by speaking with a mortgage advisor first — before they fall in love with a single property.

Quick Answer: Speak with a mortgage advisor before house hunting to understand your true budget, get pre-approved, strengthen your offers, and avoid costly surprises along the way.

Why Starting Without a Mortgage Plan Can Cost You

❶ Budget Blindspot

Falling in love with homes that are outside your actual price range.

❷ Losing Offers

Losing out to better-prepared, pre-approved buyers in a competitive market.

❸ Offer Delays

Scrambling to get financing documents together when speed matters most.

❹ Hidden Costs

Unexpected monthly payments, taxes, and cash-to-close surprises.

What Mortgage Planning Actually Looks Like

Your Advisor Helps You Understand

Your true borrowing power

Monthly payment comfort zone

Cash-to-close strategy

Loan options that fit your goals

What Is a Mortgage Pre-Approval?

A pre-approval is a formal review of your income, assets, credit history, and debt load — giving you a clear picture of how much you can borrow and at what terms.

Pro Tip

A Fully Underwritten Pre-Approval takes this a step further — underwriting is completed upfront, making you a significantly more competitive buyer when it's time to write an offer.

What You'll Need to Get Started

Pay Stubs

Most recent 30 days of employment income documentation.

W-2s or Tax Returns

Last two years of income history for a complete financial picture.

Bank Statements

One to two months of statements to verify assets and reserves.

Identification

Government-issued ID to confirm your identity during the process.

Credit Authorization

Permission to pull your credit report and assess your borrowing profile.

How Fast Can You Get Pre-Approved?

Hours

Standard pre-approval turnaround time is when documents are ready.

Step Ahead

Fully underwritten approval puts you ahead of nearly every competing buyer.

Why This Matters in a Fast Market

Move Quickly

Being fully prepared means you can act the moment the right home hits the market — no scrambling, no delays.

Write Stronger Offers

Sellers and their agents take pre-approved buyers far more seriously, especially in multiple-offer situations.

Compete Effectively

A fully underwritten pre-approval is the closest thing to a cash offer — a powerful advantage in any market.

The Bottom Line

Starting with a mortgage advisor gives you clarity, confidence, and a real competitive edge — before you ever step foot in an open house.

Mortgage Broker vs Retail Lender in Maryland: Which Is Actually Cheaper?

If you’re buying a home in Maryland, you’ll likely choose between a mortgage broker and a retail lender. Most buyers assume rates are the same everywhere—but they’re not. Choosing the right option can save (or cost) you thousands over the life of your loan.

Quick Answer: Mortgage brokers are typically cheaper than retail lenders because they access wholesale pricing and shop multiple lenders.

What Is a Retail Lender? Retail lenders fund loans directly and offer only their own rates. Their costs include higher margins, overhead, and limited pricing competition.

What Is a Mortgage Broker? A broker works on your behalf, comparing multiple lenders to find the best pricing and structure for your situation.

Real Cost Example: On a $600,000 loan, even a 0.5% rate difference can mean $200/month and $70,000+ over time.

Key Differences: Brokers offer multiple options, lower margins, faster closings, and more flexibility. Retail lenders offer one option with higher built-in costs.

Bottom Line: If your goal is to save money and win in a competitive market, a mortgage broker is typically the better option.

Ready to see the difference?

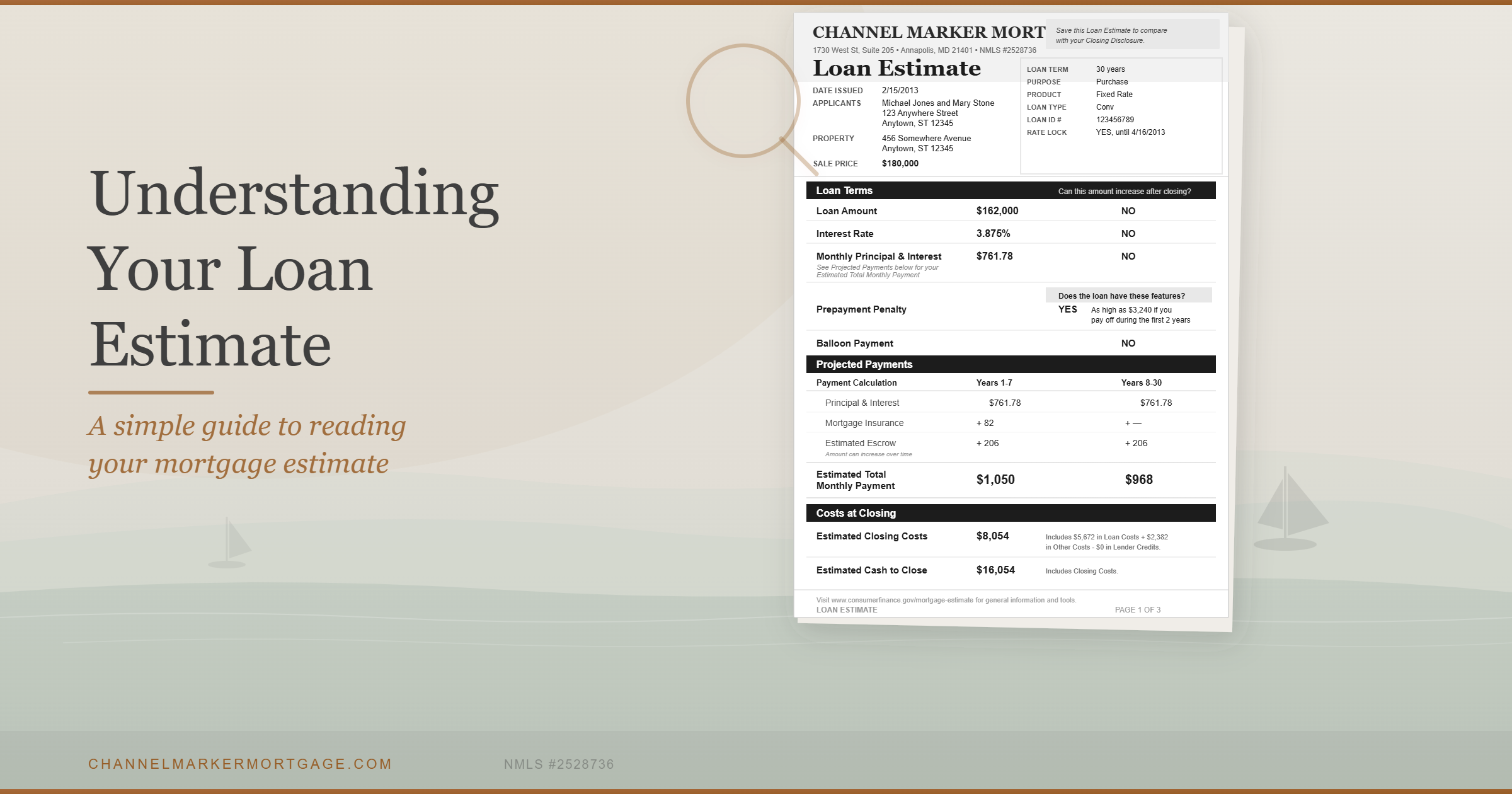

Understanding Your Loan Estimate: A Simple Guide to Reading Your Mortgage Estimate

Buying a home comes with plenty of paperwork, and one of the most important documents you’ll receive early in the process is your Loan Estimate. While it might seem complicated, this form is designed to give you a clear picture of your mortgage terms and costs before you close.

At Channel Marker Mortgage, our goal is to help you not just find the right loan, but understand every part of it. Here’s how to read your Loan Estimate with confidence.

What Is a Loan Estimate?

A Loan Estimate is a standardized, three-page document that outlines the details of your mortgage. It includes your interest rate, monthly payment, and estimated closing costs, all in a format that’s easy to compare and understand.

You’ll receive this form within three business days after applying for a mortgage. It’s meant to help you clearly see your loan terms, fees, and projected costs before you commit.

Breaking Down the Loan Estimate

Your Loan Estimate is divided into three main pages, each serving a different purpose:

Page 1: Loan Terms and Projected Payments

The first page provides a snapshot of your loan. It includes:

Loan Amount and Interest Rate

Monthly Principal and Interest

Estimated Taxes, Insurance, and Assessments

Whether your rate or payment can change over time

This page helps you understand your expected monthly payment and overall loan structure.

Page 2: Closing Cost Breakdown

Page 2 is where you’ll see a detailed breakdown of your closing costs—the total amount you’ll pay to complete your home purchase.

These costs are divided into two main sections:

Loan Costs

Fees directly related to your mortgage, including:

Origination Charges: Fees for processing and underwriting your loan.

Services You Cannot Shop For: Required services like the appraisal or credit report.

Services You Can Shop For: Title, settlement, and other third-party services you can choose.

Other Costs

Additional items that are part of the transaction, such as:

Taxes and Government Fees: Recording fees and transfer taxes.

Prepaid Items: Property taxes, homeowner’s insurance, and prepaid interest.

Initial Escrow Payments: Money set aside for future taxes and insurance.

At the bottom of this page, you’ll see your Estimated Cash to Close—the total funds you’ll need at closing, including your down payment and all applicable fees.

💡 Tip: Focus on understanding which costs are one-time (like title fees) and which are recurring (like insurance or property taxes).

Page 3: Key Disclosures and Loan Summary

The final page summarizes your loan details in one place. Here, you’ll find:

Comparisons showing what you’ll have paid in five years

The Annual Percentage Rate (APR)

Total Interest Percentage (TIP)

Lender and Loan Officer Information

This page helps you understand the total cost of your loan over time and provides contact details for your lender if you have questions.

Why It’s Important to Understand Your Loan Estimate

Your Loan Estimate isn’t just another document—it’s a roadmap to your mortgage. When you understand what you’re reading, you can make informed decisions, ask better questions, and avoid surprises at the closing table.

At Channel Marker Mortgage, we take the time to walk through your Loan Estimate line by line, ensuring you know exactly what each figure means. Our goal is clarity, not confusion.

The Loan Estimate is one of the most useful tools in the homebuying process. Once you know how to read it, you’ll feel more confident about your loan, your closing costs, and your total investment.

If you’re reviewing your Loan Estimate and want help walking through the details, our team at Channel Marker Mortgage is here to guide you, every step of the way.

Channel Marker Mortgage is a boutique mortgage lender based in Annapolis, Maryland, serving homebuyers throughout Maryland, DC, Virginia, Delaware, Pennsylvania, and Florida.

Love Where You Live: Preparing for Your Dream Home This Spring

Start planning for your dream home this February with Channel Marker Mortgage. As spring approaches, the housing market heats up, making now the perfect time to get pre-approved, prepare your finances, and secure competitive rates. Serving Maryland, DC, Virginia, Pennsylvania, and Florida, our boutique mortgage services are tailored to help you navigate the homebuying process with confidence.

February often brings thoughts of fresh beginnings and new possibilities, making it the perfect time to start planning for your dream home. With spring just around the corner, the busiest season for homebuying, there’s no better moment to prepare for your next move. At Channel Marker Mortgage, we’re here to guide you through every step of the process, ensuring you find a place you’ll love to call home for years to come.

Why February Is the Perfect Time to Start Planning

Spring is one of the most competitive seasons in the housing market, and getting ahead of the curve can make all the difference. By starting your homebuying journey in February, you’ll have time to:

Get Pre-Approved Early: A pre-approval shows sellers you’re serious and ready to make an offer. Plus, it helps you understand your budget before you start shopping.

Prepare Your Finances: February is an excellent time to review your credit, organize your savings, and create a solid financial plan.

Lock in Competitive Rates: Mortgage rates fluctuate, and starting now could help you secure a better deal before potential rate changes.

Planning ahead puts you in the best position to navigate the spring market with confidence and ease.

How to Fall in Love with Your Home Search

Finding your dream home should be an exciting journey, not a stressful one. Here are a few tips to make the process enjoyable:

Partner With Experts: Working with a knowledgeable mortgage advisor (like the team at Channel Marker Mortgage!) ensures you’re supported every step of the way.

Define Your Priorities: Make a list of your must-haves and nice-to-haves in a home. Think about location, size, features, and amenities that matter most to you.

Explore Local Charm: Especially if you’re looking in areas like Annapolis or other waterfront communities, take time to visit neighborhoods to get a feel for what makes them unique.

Budgeting Tips to Make Your Dream Home a Reality

Your budget is a key part of the homebuying process, and taking time to prepare now will set you up for success. Here are some practical steps to get started:

Save for Your Down Payment: Consider trimming unnecessary expenses, setting up automatic savings, or using your tax refund to boost your savings.

Check Your Credit Score: A higher credit score can lead to better loan options. Review your report for accuracy and take steps to improve your score if needed.

Know Your Numbers: Work with our team to assess your finances and determine how much home you can afford. We’re here to help you understand your budget and the mortgage options that best suit your needs.

Remember, every buyer’s journey is unique, and our team is here to help you create a plan tailored to your goals.

Why Choose Channel Marker Mortgage?

As a boutique mortgage lender based in Annapolis, MD, Channel Marker Mortgage is dedicated to serving clients across Maryland, DC, Virginia, Pennsylvania, and Florida with services soon expanding to Delaware. We pride ourselves on personalized guidance, competitive loan programs, and a commitment to helping you navigate the mortgage process with ease.

Ready to Fall in Love with Your New Home?

Your dream home is closer than you think, and we’d love to help you make it a reality. Whether you’re buying your first home, upgrading, or refinancing, Channel Marker Mortgage is here to guide you every step of the way.

Contact us today to schedule a consultation, and let’s start planning your spring move!